The Department of Employee Trust Funds (ETF) is responsible for administering various benefit programs available to state and local government employees. These programs include the Wisconsin Retirement System (WRS), life insurance programs for active and retired employees, and sick leave programs for retired employees.

We provided unmodified opinions on ETF’s separately issued financial statements for the following programs:

-

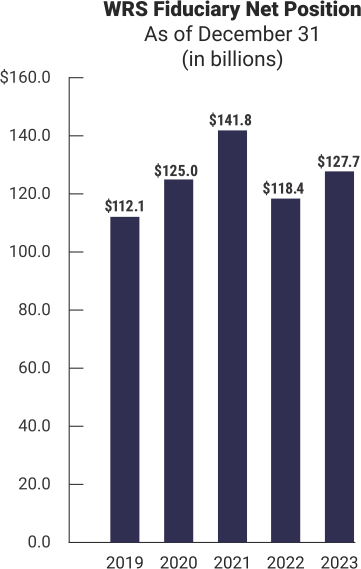

- WRS (report 24-11);

- Retiree Life insurance programs, which include the State Retiree Life Insurance program and the Local Retiree Life Insurance programs (report 24-13); and

- Supplemental Health Insurance Conversion Credit (SHICC) program (report 24-16).

For 2023, ETF again chose to separately issue its financial statements for these programs and plans to issue its 2023 Annual Comprehensive Financial Report (ACFR), which will include the financial statements of these programs as well as other programs administered by ETF, at a later date.

Employers, including the State of Wisconsin, that participate in the WRS and other postemployment benefits (OPEB) plans administered by ETF must meet specific financial reporting requirements in preparing their own financial statements using generally accepted accounting principles. To assist employers, ETF prepared employer schedules and related notes for the programs. We provided unmodified opinions on these schedules and related notes for the programs and issued the following reports:

-

- Wisconsin Retirement System Reporting for Participating Employers (report 24-12);

- State Retiree Life Insurance Reporting for the State of Wisconsin (report 24-14);

- Local Retiree Life Insurance Reporting for Participating Employers (report 24-15); and

- Supplemental Health Insurance Conversion Credit Program Reporting for Participating Employers (report 24-17).

We conducted this financial audit by auditing ETF’s financial statements and employer schedules in accordance with applicable government auditing standards, issuing our auditor’s opinions, reviewing internal controls, and issuing our auditor’s reports on internal control and compliance.