August 30, 2017

|

Pending legislation |

|

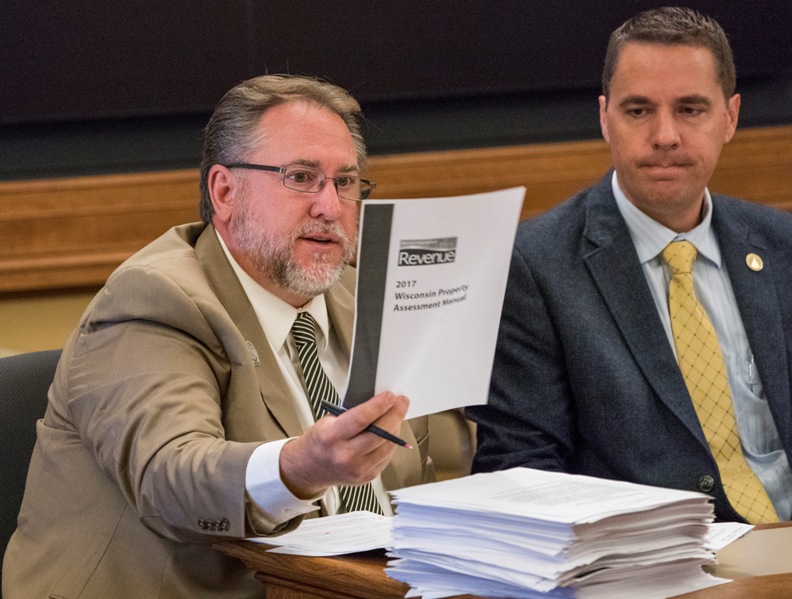

This week, municipal leaders from communities throughout Wisconsin and I, testified before the Senate Committee on Revenue, Financial Institutions and Rural Issues, on Senate Bills 291 and 292 relating to property tax assessments and closing the "Dark Store loophole." At the Assembly hearing in June, more than 55 individuals, representing cities, towns, counties, villages, and school districts, testified in favor of these proposals. Senate Bills 291 and 292 have wide bipartisan support--50 percent of legislators in both houses are cosponsors of these proposals--and were introduced at the behest of local units of government, school districts, and other political subdivisions that want to halt additional tax shifts from large retail stores to homeowners and small businesses. The litigation and tax refund costs associated with what is commonly referred to as the "Dark Store Theory," could devastate our local units of government and as such, it is imperative that a workable solution is formulated. These proposals, quite simply, clarify the best practices as proscribed by the Wisconsin Property Tax Assessment Manual. Moreover, they seek to provide clarity and direction to the Board of Review and courts when determining the value of property. The intent of these proposals is to prevent further potential tax shifts by ensuring assessments are fair and equitable for all taxpayers. Senate Bill 292, provides that, for property tax assessment purposes, to determine the value of a property using generally accepted appraisal methods, an assessor must consider all of the following as comparable to the property being assessed: 1. Sales or rentals of properties exhibiting the same or similar highest and best use with placement in the same real estate market segment. 2. Sales or rentals or properties that are

similar to the property being assessed with regard to age,

condition, use, type of construction, location, design, physical

features, and economic characteristics. The second proposal, Senate Bill 291, provides that, for property tax purposes, real property includes any leases, rights, and privileges pertaining to the property that transfer with the property shall be used in determining the value of that property. Ordinarily, the best information for assessing a property's fair-market value for property tax purposes is a recent arm's-length sale of the property. This is true in Wisconsin for all properties except single-tenant retail facilities, which have relied on the Wisconsin Supreme Court's 2008 ruling in Walgreen Company v. City of Madison, to convince courts that their assessed values should be less than half of the actual sale price of the property. A recent example of this occurred when the Wisconsin Court of Appeals relied on the aforementioned case to affirm that a single-tenant retail facility in Appleton should be valued at $1.8 million, significantly lower than the city's $4.4 million assessment, which was based on the actual sale price of the property. Appleton, a result, must now issue a $350,000 tax refund to the single-tenant retail facility.

Testifying on Senate Bills 291 and 292. Ozaukee County Fairgrounds bill This week, I also testified before the Assembly State Affairs Committee and Senate Government Operations, Technology and Consumer Protection Committee, on Assembly Bill 450 relating to: retail sales of alcoholic beverages at the Ozaukee County fairgrounds. Beginning in 2012, the Ozaukee County Board received approval from the Department of Revenue to permit licensed vendors to sell liquor on the premises of the Ozaukee County fairground for special events. The Department of Revenue made their decision to issue "Class B" permits to concessionaires based on the following state statutes: s.125.51(5)(b)2. "The department shall issue a "Class B" permit to a concessionaire that holds a valid certificate issued under s.73.03(50) and that conducts business in an operating airport or public facility, if the county or municipality which owns the airport of public facility has, by resolution of its governing body, annually applied to the department for the permit. The permit authorizes the sale of intoxicating liquor for consumption by the glass and not in the original pack or container of the premises." In 2012, the county designated concessionaires and applied for and received the necessary permits. Ozaukee County has operated under these permits since 2012 with no reported problems or complaints. Unfortunately, the Department of Revenue has recently interpreted Chapter 125 of Wisconsin state statutes differently than in 2012, resulting in Ozaukee County being prohibited from selling liquor and wine in the exposition center at the Ozaukee County fairgrounds. This decision will adversely affect future events held at the Ozaukee County fairgrounds. Assembly Bill 450, quite simply, continues the practice that permits the Ozaukee County Board to approve licensed vendors to sell liquor and wine at the Ozaukee County fairground buildings. This proposal has been vetted with the Wisconsin Tavern League and they have signed off, recognizing that permittees must be located and licensed in Ozaukee County.

Testifying with Ozaukee County officials on Assembly Bill 450. |

|

Rise in scams amid hurricane aftermath Our thoughts and prayers are with those people impacted by Hurricane Harvey. It is unfortunate that some organizations are using this tragedy to profit from the kindness and generosity of others. Please be aware of the following information from DATCP regarding the scamming of hurricane relief donations. The Wisconsin Department of Agriculture, Trade and Consumer Protection (DATCP) is urging consumers to do their research before sending money to a charity to assist those affected by Hurricane and Tropical Storm Harvey. Fake charity schemes will use any available means of soliciting "donations"--they may make their pitch over the phone, by mail, or online. They will often use names and website addresses that are nearly identical to those of major established charities, so pay close attention to the wording in a donation pitch. Keep in mind that most legitimate charity websites end in ".org" rather than ".com." Please consider the following tips to protect yourself from charity scammers:

Under Wisconsin state law, most organizations soliciting for charitable donations must register and file an annual report with the Department of Financial Institutions (DFI). To check if a charity is registered, visit the DFI website or email: DFICharitable@wisconsin.gov Coolest thing made in Wisconsin This month, Wisconsinites have the opportunity to vote on the coolest thing made in Wisconsin. Since 2012, Wisconsin has celebrated October as manufacturing month. In celebration of Wisconsin's manufacturing history and future, Wisconsin Manufacturers and Commerce is allowing individuals to vote on what is the Coolest Thing Made in Wisconsin. Nearly 300 nominations, more than 200,000 votes, and one winner. According to Wisconsin Manufacturers and Commerce, the 2016 Coolest Thing Made in Wisconsin contest was immensely popular. With last year's winner, Harley-Davidson out of the running, who will take the trophy in 2017? To determine the winner of the 2017 Coolest Thing Made in Wisconsin competition, the process will be vastly different from previous years. On August 1st, individuals began nominating products made in Wisconsin. From September 4-11, Wisconsinites will have the opportunity to narrow the products down to a field of sixteen. At that point, "Manufacturing Madness" will begin, with the first round running from September 18-25; second round October 2-6; and final round October 10-16. This tournament-style bracket will put Wisconsin products in head-to-head battles until the Coolest Thing Made in Wisconsin is announced on October 16, 2017 at the State of Wisconsin Business and Industry luncheon.

Have a great week,

Stay up to date One of the best ways to stay up to date with what is happening in Madison is to sign up for the legislature's notification tracking service. This service affords you with the opportunity to track legislative activities in Madison. Upon creation of a free account, you can sign up to receive notifications about specific bills or committees as well as legislative activity pertaining to a subject area (i.e. real estate, education, health). You can sign up for this service at any time. You can also follow me on

Facebook and

Twitter to see what

I have been doing in Madison and around the 60th Assembly

District.

Please recommend the page to your friends and family members.

|

If you would like to be removed from future mailings, email me to unsubscribe.

State Capitol Room 309 North-PO Box 8952, Madison, WI 53708

(608) 267-2369

Email: Rep.Rob.Brooks@legis.Wisconsin.gov